June 2026

Final Decision-Grade Investment Analysis

This document is a controlled internal analysis. It does not constitute an offer or external validation. It is provided under the IP Protection Notice below.

Layer A: Verifiable Facts

Corporate and legal record. Subterrane Ltd incorporated in England and Wales on 15 January 2018, company number 11149712, registered office at 17 King Edwards Road, London HA4 7AE. Certificate of incorporation issued by Companies House, Cardiff. Memorandum and Articles of Association executed on incorporation. A restructured holding entity, Subterrane Holdings Ltd, has been established offshore for IP purposes.

Intellectual property. Sigmoid Tectonics® registered as a UK trademark, number UK00003397756, filing date 8 May 2019, entered in register 18 October 2019, renewal date 8 May 2029. The registration covers an extensive range of classes spanning software, geophysical services, geological analysis, mineral exploration, educational services, and scientific research. Patent filings described as in active preparation as of June 2026.

Academic and professional record. BSc in Geology with Geophysics and MSc in Petroleum Geophysics, Imperial College London. PrSciNat registration. Prior positions at PGS (consultant geophysicist, two years), Geosoft Europe (technical analyst three years, account lead two years), and independent consulting from approximately 2015. Conference presentations accepted at the Geological Society of London (2017, 2018, 2019), Houston Potential Fields SIG (2018), AAPG, and PESGB, with a comprehensive record listed in the pitch deck appendix spanning Houston, London, Lisbon, Salt Lake City, and Johannesburg between January 2018 and May 2019.

Peer submission record. Mixed outcomes. At least one AAPG abstract was accepted with an extended abstract published in AAPG archives. A subsequent abstract, “Sigmoid tectonism: unifying plate tectonics and mantle plume theory,” was reviewed by nine referees at AAPG ACE 2019 and scored 3.94, below the selection threshold. The record establishes active pursuit of peer validation with mixed institutional outcomes.

Commercial partnership. A formal Commercial Agreement was executed on 30 January 2020 between Subterrane Ltd and Botswana Diamonds PLC (AIM and BSE listed, company number 07384657). The agreement appointed Subterrane to provide exploration services in respect of specified resources. Payment structure: upon “First Success” (defined by a weighted formula combining area, grade, and depth of burial), Botswana Diamonds would pay Subterrane direct costs of £400,000, plus ongoing commission on extraction revenues. The agreement is governed by English law. This constitutes the only executed commercial contract in the documentary record. The agreement subsequently lapsed. No First Success was reached. No commercial outcome was realised. Botswana Diamonds PLC subsequently rebranded as Botswana Minerals plc (BMIN) in February 2026 and pivoted toward copper exploration using AI-assisted analysis of its geological database, a methodology distinct from structural causality. Two RNS announcements from Botswana Minerals (formerly Botswana Diamonds PLC) confirm the partnership publicly: one announcing targets found on Thorny River, and one announcing five drill-ready targets with structures similar to the Marsfontein pipe. No payment under the agreement has been documented.

Laboratory expenditure. Two ALS Chemex South Africa invoices dated 27 November 2023, totalling USD $30,276.92 (work orders JB23288469 and JB23288475), issued to Subterrane Ltd, attentioned to Andrew Long, for rock sample analysis including crushing, splitting, pulverising, and geochemical analysis. The invoices confirm active laboratory engagement with physical samples in late 2023.

Geophysical data record. All structural interpretations rest on publicly accessible datasets — BRGM gravity, Sandwell marine gravity, EMM magnetics, Copernicus EGMS InSAR, NEOPAL neotectonics.

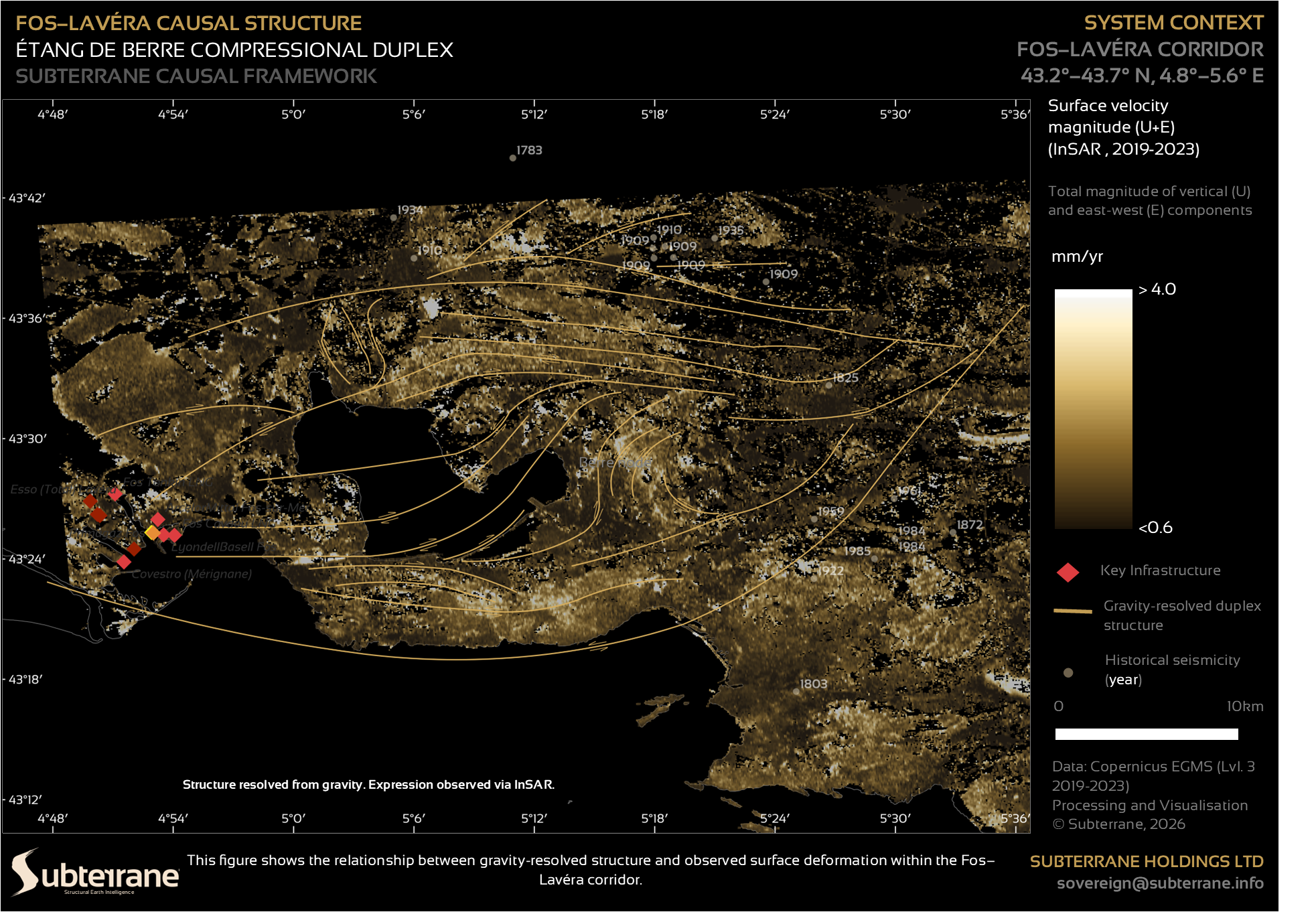

Industrial risk context. The Fos–Lavéra corridor contains approximately 35 Seveso seuil haut sites on liquefaction-prone substrate with a single RAP monitoring station. Historical earthquake losses cited align with EM-DAT and Munich Re data.

Commercial product. CIM Phase 1 is defined, priced, and commercially available at €5,000 to €30,000 per tier with delivery timelines of 5 to 30 days.

External media. A Markets Insider press release dated May 2024 covers the founder’s background and the Sigmoid Tectonics framework. This is a paid press release distribution, not editorial coverage. It does not constitute independent journalistic validation.

Investor materials. A pitch deck (July 2024), two investment teasers, and an information memorandum (IM, ref 166051, prepared by Knightsbridge PLC, Bolton) are present in the data room. The IM was produced by a third-party corporate finance firm, indicating engagement of professional advisory services for the fundraise. The financial projections contained in these materials are discussed below.

Indonesia engagement. Bob Effendi, an Indonesian industry professional, introduced the framework to professors at Institut Teknologi Bandung (ITB). Three ITB professors participated in an initial Zoom discussion in February 2026, followed by a second session in March 2026 with expanded faculty participation. An NDA was issued to ITB and remains pending within legal review. No formal validation, endorsement, or contractual engagement has been concluded.

This record constitutes documented exposure of the framework to external academic, commercial, and technical audiences. It does not constitute external validation.

The Fos–Lavéra interpretation is internally coherent across independent datasets not produced by Subterrane. BRGM gravity resolves a compressional duplex. NEOPAL paleoseismic indices align with the structural envelope. Copernicus EGMS InSAR deformation patterns organise along the same geometry. The 1909 Lambesc earthquake cluster lies on the resolved compressional limb.

The East African transform interpretation aligns with published work on strike-slip duplex systems and regional tectonics. Five kimberlite bodies in northern South Africa were reportedly identified prior to geophysical confirmation and later supported by FDEM and microdiamond sampling — consistent with the laboratory expenditure documented in the ALS Chemex invoices. The CIM node specification for Fos Cavaou LNG is formally defined with a complete mathematical transformation chain.

The Botswana Minerals plc (formerly Botswana Diamonds PLC) RNS announcements confirm that a public AIM-listed company, assessed and advised by qualified geologists with over 33 years of industry experience, was prepared to state publicly that Subterrane’s methodology had identified five drill-ready targets with structures similar to Marsfontein. This is the strongest independent corroboration in the documentary record. It is not scientific validation of the methodology. It is commercial endorsement of the targeting outputs by a qualified external party with reputational and regulatory accountability.

None of this has undergone external scientific review. It exceeds assertion but remains unverified.

That gravity encodes a causal flow structure governing fault connectivity, seismic release, and resource emplacement at the level claimed. That this can be systematised into a repeatable, auditable product independent of founder judgment. That the CIM scalar can function as a pricing primitive. That institutions will pay for structural state measurement. That M1 corridor diamond targets are economic-grade. That the Nine Sovereign Instruments are legally constructible.

Critical Boundary

Layer B establishes pattern coherence and, through the BOD partnership and RNS record, one instance of qualified external commercial endorsement of targeting outputs. It does not establish predictive determinism, economic viability, or pricing power. The transition from B to C is the investment risk. Conflation produces either over-extension or premature dismissal. The boundary is load-bearing and remains explicit.

Absence of prior adoption is not disproof.

Global gravity datasets at structurally useful resolution became widely available after approximately 2014–2015, following improvements in satellite-derived gravity and global magnetic models. Earlier datasets lacked sufficient resolution and stability for this class of interpretation.

The binding constraint was economic. Gravity was treated as a residual anomaly to be inverted, not as a structural system to be interpreted. Commercial geophysics optimised for hydrocarbon workflows and short-cycle deliverables. Structural reinterpretation did not align with these incentives.

Catastrophe finance exhibits a parallel constraint. Pricing frameworks depend on probabilistic uncertainty. Measurement that compresses uncertainty compresses margins. There has been limited incentive to build causal measurement infrastructure from within the system it would disrupt.

Peer reception has been mixed rather than confirmatory. This establishes attempted external validation and inconclusive outcomes. It does not resolve validity.

The absence of adoption is contextually explicable. It is not evidentiary.

The data room contains financial models across multiple documents. The information memorandum (166051) produced by Knightsbridge PLC projects Year 1 EBITDA of $50.4M at a 66% margin from mining revenue. The investor model and pitch deck contain comparable projections. These figures require precise contextual treatment.

The projections are professionally prepared in the sense that a third-party corporate finance firm was engaged to produce the IM. They are not independently audited. They are revenue projections for a pre-revenue mining company based on assumptions about discovery grade, mine economics, and production timelines that cannot be validated before drilling occurs.

The Year 1 EBITDA figure implies rapid transition from license acquisition to producing mine with economic-grade output — a sequence that industry experience places at a minimum of 12 to 36 months under favourable conditions. The projections should be treated as illustrative of the maximum upside case under optimal assumptions, not as a base case or a forecast. They are appropriate for a marketing context. They are not appropriate as the basis for an investment decision.

What the financial model does confirm: the internal logic of the opportunity, if the geology holds, produces substantial margins. Marsfontein-type shallow blow pipes have historically operated at very high margins due to minimal processing requirements. The economic model is coherent if the geological premise is correct. Whether the geological premise is correct is what the drill test resolves.

Resolution occurs through externally observable tests. Each component has a failure condition and a continuation signal.

| Component | Kill Condition | Continue Signal |

|---|---|---|

| CIM methodology | Independent teams cannot reproduce node outputs from public datasets within tolerance | One paying industrial client with no personal relationship to the founder, plus repeat engagement or referral |

| Diamond thesis | Initial M1 corridor drill targets return sub-economic grades with no macrodiamond recovery above background | Recovery above background levels, irrespective of immediate economic viability |

| Structural lens | No measurable correlation between predicted corridors and independent deformation or seismic data over a defined window | Alignment between predicted geometry and independent deformation data |

| Independent reproduction | Third-party inability to replicate Fos–Lavéra or East African structural interpretations | Partial structural replication |

All four tests are executable within 12 to 24 months without full capital deployment.

The diamond arm now has a documented commercial history that upgrades it from a theoretical premise.

A formal agreement with an AIM-listed company was executed and publicly announced. A qualified geologist with over 33 years of diamond sector experience assessed the targets and was prepared to state publicly that five drill-ready targets had been identified. Laboratory expenditure of over $30,000 on rock sample analysis in late 2023 confirms continued physical engagement with the ground after the BOD partnership period.

The commercial outcome — no payment under the agreement, no production — remains the critical fact. But the documentary record now establishes that the targeting methodology produced outputs that a publicly accountable external party endorsed and announced to regulated markets. That is a meaningfully stronger position than unvalidated internal claim.

At approximately $350,000, the test yields high information relative to cost. Industry base rates imply low probability of immediate economic discovery. Timeline to economic confirmation is 12 to 36 months with follow-on capital. Financial projections are illustrative, not predictive. Value lies in information, not early cash flow.

Decision variable: information yield per unit capital.

| Test | Capital | Information Yield |

|---|---|---|

| Diamond drilling (M1 corridor) | ~$350,000 | High — geological validation with prior BOD endorsement context |

| CIM Phase 1 commercial conversion | €5,000–30,000 | High — market validation |

| Atlas corridor products | €250–€3,500 | Immediate revenue validation |

| Independent reproduction | Low | High — method validation |

| Vessel phase | $30–50M | Conditional |

| Sovereign instruments | $100M+ | Dependent |

Early capital should resolve uncertainty. The first three tests determine whether further deployment is rational.

CIM Phase 1 requires no proprietary data acquisition, targets high-liability assets, operates adjacent to existing systems, and requires limited conceptual adoption.

Progression: baseline mapping → repeatability → workflow integration → financial layer.

Commercial validation is absent. No confirmed paying client exists. This remains the primary unresolved condition.

The constraint is structural. Causal measurement compresses information asymmetry embedded in current pricing models. Adoption depends on external pressure rather than intrinsic superiority. Incumbents are disincentivised to adopt early. If validated, advantage accrues to early movers outside incumbent structures.

Internal coherence is non-diagnostic.

Two states are observationally identical: coherent but incorrect, and coherent but unvalidated. Mixed peer outcomes and the BOD commercial history do not resolve this. The BOD endorsement confirms that qualified external parties found the targeting outputs credible enough to announce publicly. It does not confirm that the underlying interpretive framework is scientifically valid.

Resolution requires external constraint: market (payment), matter (drill), method (independent reproduction). Absent these, coherence remains a property of construction, not validation.

Seven years without a commercially monetised outcome produces three possible conditions.

Access failure — valid product, distribution constraint. The BOD partnership history suggests this is partially operative: targets were identified and endorsed, but the partnership did not produce payment. Whether that reflects BOD’s operational and financial constraints or a limitation of the commercial model is not determinable from the record.

Translation failure — signal exists but is not communicable in a form that drives commercial action. The rhetorical register of the Deep Frontier series and the scale of the vision may create friction with industrial operators whose decision cycles are shorter.

Method failure — the system does not produce external value at the level required for payment. The BOD RNS record partially mitigates but does not eliminate this possibility.

All three produce identical observable outcomes. Differentiation requires external tests.

The thesis resolves sequentially.

Signal exists — scientific validity — is the foundation. If this fails, nothing downstream is accessible.

Signal is non-commoditised — market gap — enables a position. The BOD partnership confirms the targeting outputs are commercially differentiated enough for a regulated company to announce them publicly.

Signal is systematisable — scalability — determines whether the business scales beyond a single-practitioner operation. This is the critical transition and the point most exposed to epistemic closure risk.

Signal is monetisable — commercial adoption — is the realisation. The BOD agreement was structured for contingent payment on First Success. First Success was not documented. The monetisation pathway has been defined and tested. It has not yet completed.

Failure propagates forward. Success compounds forward.

Appropriate under conditions of high uncertainty, staged deployment, and tolerance for binary outcomes within a defined validation window.

Not appropriate where prior validation, near-term cash flow, or institutional constraints are required.

The system is coherent, structured, and grounded in real datasets applied over a decade of field and analytical work. The corporate record is clean: incorporated 2018, trademark registered 2019, commercial agreement executed with a regulated public company in 2020, laboratory expenditure confirmed in 2023, CIM product defined and commercially available in 2026.

The documentary record adds one element not previously visible in the analysis: a qualified independent party — a publicly listed company advised by a 33-year diamond sector specialist — assessed the targeting outputs, found them sufficiently credible to commit to a commercial agreement and announce targets to regulated markets. This is the strongest external corroboration in the record. It did not produce payment. The reason is undocumented.

No recurring commercial revenue has yet been established.

The opportunity is defined by capital-efficient testability within a 12 to 18 month window. Three external constraints are required: a drill result to introduce matter, a paying client to introduce market, and an independent reproduction to introduce method. Total capital to force these tests: sub-$500,000.

Before these occur, distinction between breakthrough and false positive remains indeterminate. After one occurs, resolution begins.

Pipeline signals exist. One qualified external endorsement of targeting outputs exists, without payment. Atlas corridor products introduce a lower-cost commercial validation pathway that did not exist in earlier versions of the strategy.

The investment question is procedural: whether to fund the minimum set of tests required to force that resolution.

IP Protection Notice

CIM, the Causality Lens™, Sigmoid Tectonics®, and the Nine Sovereign Instruments constitute proprietary intellectual property of Subterrane Holdings Ltd. International IP protection strategy and patent filings are in active preparation. The underlying causal architecture predates formal CIM publication and is evidenced by continuous prior-art record from 2015 onward. Prior-art publication is established across The Deep Frontier dispatch series (May 2025–present) and associated technical papers (2019–2025). All rights reserved. Unauthorised use, reproduction, or derivative commercial application is prohibited. Engagement establishes controlled disclosure under commercial review.